![]()

Edge AI Hardware Market Research Report Information by Edge Layer (MicrEdge, Deep Edge, and Meta Edge), By Processor Type (CPUs (AI-optimized), GPUs (Edge GPUs)

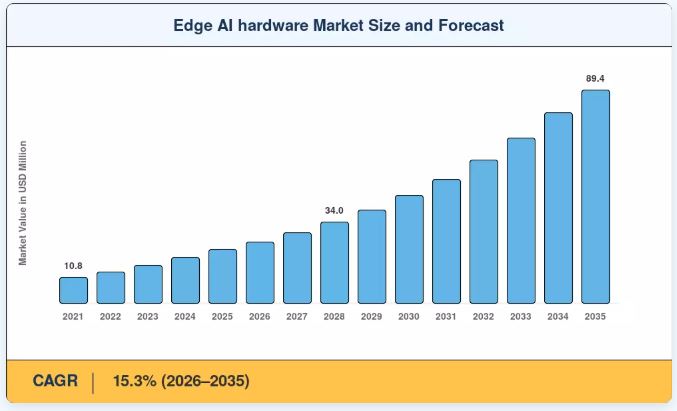

NEW YORK,, CA, UNITED STATES, June 15, 2026 /EINPresswire.com/ — The Global Edge AI Hardware market was valued at USD 22.6 billion in 2025 and is projected to grow from USD 25.8 billion in 2026 to USD 89.4 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 15.3% during the forecast period. The explosive proliferation of Internet of Things (IoT) ecosystems, the accelerating rollout of 5G network infrastructure, and the critical enterprise demand for low-latency, real-time data processing at the network edge are collectively transforming Edge AI hardware into the foundational computing layer of the modern digital economy.

By shifting intelligence from centralized cloud data centers directly onto local devices and edge nodes, these solutions enable faster autonomous decision-making, enhanced data privacy, and significant reductions in bandwidth consumption across every major industry vertical.

The transition from cloud-centric AI inference to distributed edge intelligence represents one of the most consequential architectural shifts in the history of computing. Mission-critical applications including autonomous vehicles, surgical robotics, real-time industrial quality control, and smart grid management demand sub-millisecond latency and continuous operation that cloud dependency cannot reliably deliver. Simultaneously, growing data sovereignty regulations across the EU, Asia-Pacific, and emerging markets are compelling enterprises to adopt on-premise and edge-based AI processing to meet compliance obligations, creating a powerful regulatory tailwind for the market.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://www.marketresearchfuture.com/sample_request/7836

✿ How Significant Is the Edge AI Hardware Market’s Growth?

The scale of this growth reflects the breadth of end markets being transformed by edge AI capabilities. Automotive ADAS and autonomous driving systems, industrial automation and smart manufacturing platforms, healthcare diagnostics and patient monitoring devices, smart city surveillance infrastructure, and consumer electronics incorporating on-device AI assistants are all generating sustained, high-value demand for processors, neural processing units (NPUs), GPUs, ASICs, and FPGAs optimized for edge inference workloads. The hardware market is the foundational enabler upon which this entire application ecosystem is built.

✿ What Does the Future Hold for the Edge AI Hardware Market?

Purpose-built AI silicon stands at the center of the market’s next growth phase. Application-specific integrated circuits (ASICs) and neural processing units (NPUs) designed specifically for edge AI inference workloads are displacing general-purpose CPUs in performance-sensitive and power-constrained applications. Companies including NVIDIA, Google, Apple, Qualcomm, and a new generation of AI chip startups are competing intensely to define the dominant edge inference architectures for automotive, mobile, industrial, and IoT platforms.

The convergence of 5G, edge computing, and AI is creating a new computing paradigm known as the “intelligent edge.” As 5G private networks proliferate across factory floors, logistics hubs, and smart city deployments, edge AI hardware embedded in network equipment and local servers is enabling real-time AI-driven automation at scale without cloud round-trip latency. This convergence is driving a new wave of enterprise infrastructure investment expected to accelerate significantly through 2030.

Power efficiency is emerging as a critical competitive battleground. As edge AI workloads are deployed across battery-powered IoT sensors, wearables, and mobile devices, the ability to deliver maximum AI inference performance per watt is becoming a primary hardware design requirement. Advances in semiconductor process nodes (3nm and beyond), in-memory computing architectures, and neuromorphic chip designs are enabling order-of-magnitude improvements in energy efficiency that are unlocking entirely new categories of edge AI applications.

✿ Who Are the Key Players in the Edge AI Hardware Market?

The Edge AI hardware landscape is characterized by intense competition among established semiconductor giants, hyperscale technology companies developing proprietary AI silicon, and a dynamic ecosystem of specialized AI chip startups. Key participants shaping the competitive dynamics include:

➤NVIDIA Corporation — the dominant force in AI accelerator hardware, with its Jetson edge AI platform providing GPU-based inference solutions for robotics, autonomous machines, and industrial edge applications.

➤Intel Corporation — offering a broad portfolio of edge AI hardware including the Movidius Neural Compute Stick, OpenVINO-optimized processors, and Gaudi AI accelerators targeting edge inference deployments.

➤Google (Alphabet Inc.) — driving edge AI adoption through its Coral Edge TPU hardware platform and on-device AI capabilities embedded across Pixel consumer devices and Nest smart home products.

➤Qualcomm Incorporated — a leading provider of mobile and IoT edge AI silicon through its Snapdragon platform, powering on-device AI in smartphones, wearables, automotive systems, and industrial IoT devices.

➤Apple Inc. — setting the benchmark for consumer edge AI hardware with its proprietary Neural Engine integrated into A-series and M-series chips, enabling advanced on-device AI across iPhone, iPad, and Mac platforms.

➤Samsung Electronics Co., Ltd. — a major supplier of application processors with integrated NPU capabilities for mobile and consumer IoT devices, alongside memory solutions critical for edge AI performance.

➤Huawei Technologies Co., Ltd. — a significant player in edge AI hardware through its Ascend AI chip family and HiSilicon Kirin mobile processors, with strong presence across China and emerging markets.

➤ARM Holdings — providing the foundational CPU and NPU IP architectures licensed by the vast majority of edge AI chip designers globally, making it a pivotal enabler of the entire edge AI hardware ecosystem.

➤Hailo Technologies — an AI chip startup delivering purpose-built edge AI processors with industry-leading performance-per-watt metrics for smart cameras, automotive ADAS, and industrial vision applications.

➤MediaTek Inc. — supplying integrated AI processing solutions for mid-range smartphones, smart displays, connected home devices, and automotive infotainment systems across high-volume emerging markets.

➤IBM Corporation — advancing neuromorphic and analog AI chip research through its NorthPole architecture, targeting ultra-energy-efficient edge inference for enterprise and IoT applications.

➤Xilinx Inc. (AMD) — providing FPGA-based adaptive computing platforms that enable flexible, reprogrammable edge AI inference for industrial, automotive, and communications applications.

Strategic competition in this market centers on silicon performance benchmarks, power efficiency profiles, software ecosystem depth, and the ability to support end-to-end MLOps workflows from cloud training to edge deployment.

✿ What Are the Emerging Trends in the Edge AI Hardware Market?

Several transformational trends are redefining how the Edge AI hardware market evolves through 2035:

Purpose-Built NPU & ASIC Proliferation: General-purpose CPU and GPU architectures are being supplemented and in many workloads supplanted by task-specific neural processing units and custom ASICs delivering superior inference performance and energy efficiency for targeted edge AI applications including computer vision, natural language processing, and predictive analytics.

On-Device Generative AI: The migration of large language model (LLM) inference onto edge hardware enabled by model quantization, pruning, and distillation techniques is creating a new high-performance segment within the edge AI hardware market. Smartphones, AI PCs, and edge servers capable of running compressed generative AI models locally represent a fast-growing category.

Automotive AI Silicon Expansion: The transition to software-defined vehicles and the proliferation of ADAS Level 2+ to Level 4 autonomous driving systems are generating exceptional demand for high-performance, safety-certified AI SoCs. Automotive-grade edge AI silicon is among the fastest-growing hardware segments within the broader market.

Industrial Edge AI & Industry 4.0: Smart manufacturing deployments integrating computer vision quality inspection, predictive maintenance analytics, and autonomous robotic systems are driving strong enterprise hardware procurement cycles across North America, Europe, and Asia-Pacific.

Tiny ML & Ultra-Low-Power Edge Inference: TinyML frameworks enabling AI inference on microcontrollers consuming milliwatts of power are unlocking edge AI capabilities in battery-powered sensors, medical wearables, and agricultural monitoring devices dramatically expanding the addressable hardware market into billions of constrained IoT endpoints.

Sovereign AI & Domestic Semiconductor Investment: Geopolitical technology competition and CHIPS Act-style subsidy programs across the US, EU, India, Japan, and South Korea are accelerating domestic edge AI chip development and manufacturing capacity investment, reshaping global supply chains and competitive dynamics in the hardware market.

Get access to the full description of the report @

https://www.marketresearchfuture.com/reports/edge-ai-hardware-market-7836

✿ How Is the Edge AI Hardware Market Segmented?

The Edge AI hardware market report provides a comprehensive segmentation framework:

By Component: CPU, GPU, ASIC, FPGA, Neural Processing Unit (NPU)

By Device Type: Smartphones, Cameras, Robots, Wearables, Smart Speakers, Industrial Edge Servers, Other Devices

By Application: Inference, Training

By End-Use Industry: Automotive & Transportation, Healthcare, Industrial & Manufacturing, Consumer Electronics, Retail, Energy & Utilities, Smart Cities & Infrastructure, Defense & Aerospace

By Region: North America, Europe, Asia-Pacific, Middle East & Africa, South America

✿ What Are the Regional Insights from the Edge AI Hardware Market?

North America commands the largest share of the global Edge AI hardware market, accounting for over 36% of revenues. The United States is the primary driver, anchored by the presence of the world’s leading AI chip designers NVIDIA, Intel, Qualcomm, Apple, and Google alongside massive enterprise adoption of edge AI across automotive, healthcare, defense, and industrial sectors. Significant federal investment in semiconductor manufacturing through the CHIPS and Science Act is further reinforcing North America’s competitive position in AI hardware development and production.

Europe holds the second-largest regional share, driven by strong automotive AI hardware demand from Germany’s premium vehicle manufacturers, industrial edge AI adoption across the region’s advanced manufacturing base, and regulatory frameworks such as the EU AI Act and GDPR that are incentivizing on-premise and edge-based AI processing over cloud-dependent architectures. EU semiconductor sovereignty initiatives and investment in domestic AI chip research are building longer-term regional supply chain resilience.

Asia-Pacific represents the fastest-growing regional market for edge AI hardware, fueled by China’s massive domestic AI semiconductor industry led by Huawei HiSilicon, Cambricon, and Horizon Robotics alongside strong demand growth in South Korea, Japan, Taiwan, and India. China’s government-backed push to achieve AI chip self-sufficiency, combined with the world’s largest smartphone and consumer electronics production base, makes Asia-Pacific the dominant volume market for edge AI silicon through 2035.

The Middle East & Africa and South America regions, while currently representing smaller revenue shares, are projected to register above-average growth rates driven by smart city infrastructure investment, mobile-first AI application adoption, and government digital transformation programs in Saudi Arabia, the UAE, Brazil, and India that prioritize edge computing and sovereign data processing capabilities.

➤➤➤ Regional & Country-Level Reports by Market Research Future:

China Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/china-edge-ai-hardware-market-46827

Germany Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/germany-edge-ai-hardware-market-46824

India Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/india-edge-ai-hardware-market-46826

Japan Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/japan-edge-ai-hardware-market-46825

South Korea Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/south-korea-edge-ai-hardware-market-46823

Us Edge Ai Hardware Market

https://www.marketresearchfuture.com/reports/us-edge-ai-hardware-market-14097

➤➤➤ Industry Analysis Reports by Market Research Future:

Industrial Agitator Market-

https://www.marketresearchfuture.com/reports/industrial-agitator-market-5396

Smart Grid Sensors Market-

https://www.marketresearchfuture.com/reports/smart-grid-sensors-market-5427

X-Ray Inspection Systems Technology Market-

https://www.marketresearchfuture.com/reports/x-ray-inspection-systems-technology-market-5430

Gas Sensor Market-

https://www.marketresearchfuture.com/reports/gas-sensors-market-5459

Total Stations Market-

https://www.marketresearchfuture.com/reports/total-stations-market-5727

Sagar Kadam

Market Research Future

+ +1 628-258-0071

email us here

Visit us on social media:

LinkedIn

Facebook

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery